Luxury cruise travel insurance is specialized coverage designed to protect against the expensive and unique risks of high-end maritime vacations, including medical emergencies at sea, trip interruptions, and lost high-value personal items. Standard travel policies fall short for voyages on lines like Regent Seven Seas, Silversea, or Seabourn, where a single itinerary can exceed $30,000 per person. This luxury cruise travel insurance guide covers what to prioritize, when to buy, how much to spend, and which plan types deliver real protection. Providers like Squaremouth and plans like iTravelInsured LX exist specifically for travelers whose financial exposure demands more than a generic policy.

What coverage should luxury cruise travelers prioritize?

The right coverage for a luxury voyage starts with medical and evacuation limits that match the actual cost of a maritime emergency. Medical evacuations from remote regions can cost between $150,000 and $500,000 or more. That means a policy with a $50,000 medical limit is not just inadequate. It is a financial liability.

Here are the core coverage categories every luxury cruise traveler should verify before purchasing:

- Emergency medical coverage: Minimum $100,000, with $500,000 or more strongly preferred for remote itineraries like Antarctica, the Arctic, or the South Pacific.

- Medical evacuation: Aim for at least $500,000 to $1,000,000. Evacuation limits at this level are standard in specialized plans like iTravelInsured LX, which is built specifically for high-value voyages.

- Trip cancellation and interruption: Should cover 100% of non-refundable prepaid costs, including flights, hotel stays, and pre-booked excursions.

- Cancel For Any Reason (CFAR): This optional upgrade lets you cancel for reasons not listed in the base policy and typically reimburses 50%–75% of trip costs. It is the most flexible protection available for travelers with uncertain schedules.

- Baggage and valuables: Standard policies carry single-item limits of only $300–$500. If you travel with jewelry, cameras, or designer goods, you need a rider that specifically covers those items at their full replacement value.

- Cruise-specific benefits: Look for missed ship departure coverage, itinerary change protection, and shipboard quarantine reimbursement. These are unique maritime risks that generic policies do not include.

Pro Tip: Read the exclusions section of any policy before the benefits summary. Insurers bury the most important limitations there, not in the headline coverage amounts.

How much does luxury cruise insurance typically cost?

Luxury cruise insurance costs between 4% and 10% of total non-refundable trip expenses. That range is wide because several variables push premiums up or down significantly.

| Trip Value | Standard Policy (6%) | With CFAR Upgrade (+45%) |

|---|---|---|

| $10,000 | $600 | $870 |

| $20,000 | $1,200 | $1,740 |

| $40,000 | $2,400 | $3,480 |

| $60,000 | $3,600 | $5,220 |

Three factors drive most of the cost variation. First, the total insured trip value is the biggest lever. Second, traveler age matters significantly because insurers price medical risk by age bracket, and premiums for travelers over 70 can run toward the top of the 4%–10% range. Third, trip duration adds exposure days, which increases the likelihood of a claim.

CFAR upgrades add 40%–50% to base premiums. That is a real cost, but for a $40,000 voyage, the difference between recovering nothing and recovering 75% of your trip cost is worth the math. Third-party providers accessed through comparison platforms like Squaremouth consistently offer better coverage value than cruise line insurance packages, which tend to carry lower limits at higher prices.

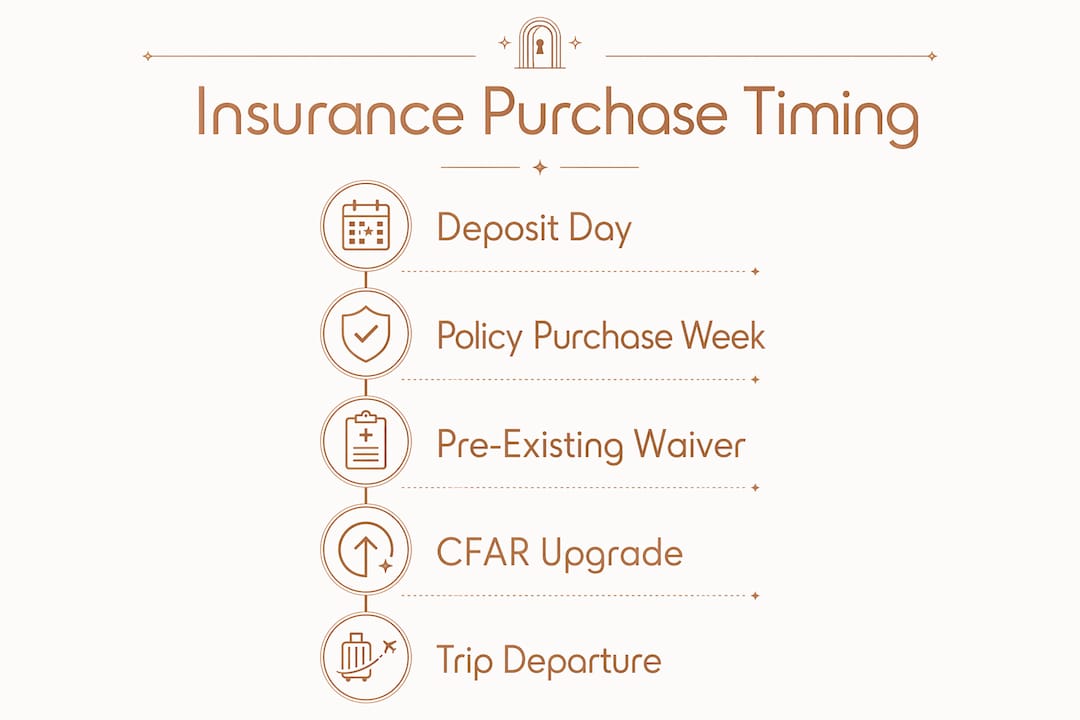

When is the best time to buy cruise travel insurance?

The best time to purchase cruise travel insurance is within 14–21 days of your initial trip deposit. This is not a suggestion. It is the trigger point for two of the most valuable protections in any policy.

Here is why timing controls your coverage quality:

- Pre-existing condition waivers activate at purchase. Buying within 14–21 days of your deposit is the standard window to qualify for a waiver that covers medical claims related to pre-existing conditions. Miss that window and those conditions are excluded.

- Cancellation coverage is retroactive to purchase date. If you wait until two weeks before sailing and a family emergency forces you to cancel, you have no coverage for the months of prepaid costs that accumulated before you bought the policy.

- Nearly 40% of cruise travelers buy insurance late. Research shows that a large share of travelers delay purchase, which directly invalidates cancellation and pre-existing condition protections they assumed they had.

- Cruise lines can deny boarding without proof of coverage. Some luxury lines require travelers to present proof of adequate medical and evacuation insurance at embarkation. Arriving without it can mean missing your voyage entirely.

- Early purchase covers the full trip ecosystem. Flights booked months in advance, pre-cruise hotel nights, and shore excursions paid upfront are all at risk until you have a policy in place.

Pro Tip: Set a calendar reminder for the day after you pay your cruise deposit. Purchase your policy that same week. Waiting even a month can cost you the most valuable protections in the plan.

Cruise-specific vs. generic travel insurance: which is better?

Cruise-specific insurance plans are the superior choice for luxury maritime travel. Generic travel policies are built for land-based trips and leave critical gaps when applied to voyages at sea.

| Coverage Feature | Cruise-Specific Plan | Generic Travel Policy |

|---|---|---|

| Missed ship departure | Included | Rarely included |

| Shipboard quarantine costs | Included | Not included |

| Itinerary change protection | Included | Not included |

| Medical evacuation limits | $500,000–$1,000,000+ | $100,000–$250,000 typical |

| Cruise interruption benefits | Included | Not included |

| Pre-existing condition waiver | Available with early purchase | Often excluded entirely |

Third-party cruise plans offer higher medical and evacuation limits and more flexible cancellation policies than cruise line packages. Cruise line insurance is convenient to purchase at booking, but it is designed to protect the cruise line’s revenue, not your full financial exposure. A traveler on a luxury expedition cruise to the Galápagos or Norwegian fjords faces evacuation scenarios that a cruise line policy simply is not built to handle.

Specialized plans like iTravelInsured LX are designed from the ground up for high-value voyages. They include stronger evacuation limits, cruise interruption coverage, and higher baggage sub-limits than anything a cruise line’s own insurance desk will offer.

How to evaluate cruise insurance plans and avoid common mistakes

Choosing the right plan requires more than comparing headline prices. The most expensive policy is not always the best one, and the cheapest will almost certainly leave gaps.

What to check in any policy:

- Confirm the medical evacuation limit is at least $500,000 for remote itineraries

- Verify that the baggage section includes a rider or endorsement for high-value items

- Check whether adventure activities like snorkeling, kayaking, or helicopter excursions are covered or excluded

- Confirm the policy covers your specific destinations, including any countries under travel advisories

- Read the definition of “trip interruption” carefully. Some policies only cover interruptions caused by a narrow list of named events

Common mistakes luxury cruise travelers make:

- Waiting until the week before departure to purchase, which voids pre-existing condition waivers and retroactive cancellation protection

- Relying on cruise line insurance without comparing it to third-party options

- Ignoring single-item baggage limits and discovering after a loss that a $5,000 watch was only covered for $300

- Skipping CFAR on high-cost voyages where personal or business circumstances could realistically force a cancellation

Understanding insurance choices for luxury trips requires reading policies at the clause level, not just the summary page. If you are comparing plans on Squaremouth or a similar platform, filter first by evacuation limit, then by CFAR availability, then by price.

Key takeaways

Comprehensive cruise-specific insurance with high evacuation limits, early purchase timing, and valuables riders is the only reliable protection for a luxury cruise investment.

| Point | Details |

|---|---|

| Buy within 14–21 days of deposit | This window activates pre-existing condition waivers and retroactive cancellation coverage. |

| Prioritize evacuation limits | Aim for $500,000–$1,000,000 in evacuation coverage for any remote or expedition itinerary. |

| Choose cruise-specific plans | Plans like iTravelInsured LX include maritime protections that generic policies exclude entirely. |

| Add valuables riders | Standard single-item limits of $300–$500 are insufficient for luxury travelers carrying high-value goods. |

| Compare third-party providers | Platforms like Squaremouth consistently surface better value than cruise line insurance desks. |

What i’ve learned after years of booking luxury cruises

The single most expensive mistake I see luxury travelers make is treating insurance as an afterthought. They spend months selecting the right suite on the right ship, then spend 10 minutes choosing a policy the week before departure. That sequence is backwards.

Medical evacuation from a remote destination is not a theoretical risk. It is a real scenario that plays out every season, and the costs are not negotiable. A helicopter transfer from a remote fjord or a medivac flight from the South Pacific can easily exceed $300,000. I have seen travelers return from extraordinary voyages carrying debt they did not expect because their policy limit was $100,000 and their bill was three times that.

My strong recommendation is to work with a specialized travel agency that understands the insurance landscape for high-value trips. Generic policies sold at checkout are not built for your exposure level. The right broker or advisor will match your specific itinerary, health profile, and trip value to a plan that actually covers what you need.

Price should be the last filter, not the first. A $500 difference in premium is irrelevant if the cheaper policy has a $250,000 evacuation cap and you are sailing to Antarctica. Look at coverage quality and insurer reputation before you look at cost.

— Michael

Plan your luxury cruise with confidence

Securing the right insurance is one part of building a truly protected luxury voyage. Hiddendoortravel specializes in bespoke cruise planning for discerning travelers who expect every detail handled correctly, including the coverage that protects their investment before the ship even leaves port.

The team at Hiddendoortravel works with clients to match itineraries, manage pre-trip logistics, and identify the right insurance framework for each voyage. Whether you are planning a first expedition cruise or your tenth world voyage, our luxury travel experts are ready to help you build a trip worth protecting. Reach out to start planning a voyage designed around your standards.

FAQ

What is the minimum medical coverage for a luxury cruise?

Emergency medical coverage of at least $100,000 is the baseline, but $500,000 or more is strongly recommended for remote or expedition itineraries where evacuation costs alone can exceed $300,000.

Does cruise travel insurance cover pre-existing conditions?

Most cruise-specific plans offer a pre-existing condition waiver if you purchase the policy within 14–21 days of your initial trip deposit. Buying late typically excludes those conditions entirely.

Is cruise line insurance as good as third-party plans?

Third-party plans consistently offer higher limits and better value than cruise line insurance packages. Cruise line policies tend to carry lower evacuation limits and more restrictive cancellation terms.

What does CFAR coverage add to a cruise insurance policy?

Cancel For Any Reason coverage lets you cancel for reasons not listed in the base policy and typically reimburses 50%–75% of trip costs. It adds 40%–50% to base premiums but offers the most flexible cancellation protection available.

Do i need a special rider for jewelry and valuables on a cruise?

Standard baggage policies carry single-item limits of $300–$500, which is far below the value of most luxury travelers’ personal items. A valuables rider is necessary to cover jewelry, cameras, or designer goods at their actual replacement value.