You spend months planning a private safari, a Mediterranean yacht charter, or a bespoke villa stay in Tuscany. The deposits are paid, the itinerary is locked, and the anticipation is real. Then something goes wrong. The role of travel insurance in luxury travel is not about covering a budget shortfall. It is about protecting tens of thousands of dollars in prepaid, non-refundable expenses, securing world-class medical care if the unexpected happens, and having a team of experts ready to untangle a complex itinerary at 2 a.m. in a foreign country. If you have ever thought of travel insurance as optional, this guide will change that.

Table of Contents

- Key takeaways

- The role of travel insurance in luxury travel

- Medical and evacuation coverage abroad

- Cancel For Any Reason: flexibility with fine print

- Concierge and assistance services

- Selecting luxury travel insurance

- My perspective on what insurance actually does for luxury travelers

- Plan your luxury trip with the right protection in place

- FAQ

Key takeaways

| Point | Details |

|---|---|

| High trip costs demand coverage | Luxury insurance typically costs 4–10% of trip expenses but can recover 100% of non-refundable bookings. |

| Medical limits must be high | Top luxury plans offer $250,000+ in medical coverage and up to $1,000,000 for evacuation. |

| CFAR requires early action | Cancel For Any Reason coverage must be purchased within 14–21 days of your initial deposit. |

| Concierge services matter | 24/7 multilingual assistance coordinates rebookings, medical logistics, and lost document recovery. |

| Insure the full trip cost | Partial coverage invalidates CFAR eligibility and leaves expensive prepaid components unprotected. |

The role of travel insurance in luxury travel

Luxury trips are not like standard vacations. The financial exposure is categorically different. A two-week private tour of Japan with first-class flights, ryokan stays, and curated experiences can easily exceed $40,000 per couple. A chartered yacht in the Greek islands or a polar expedition to Antarctica can run well beyond that. Luxury insurance policies typically cost 4–10% of total trip expenses, with that pricing reflecting exactly what is at stake: the full recovery of substantial prepaid, non-refundable costs.

The misconception that insurance is an unnecessary luxury add-on collapses the moment you look at what these policies actually do. Standard travel insurance handles the basics. Luxury trip insurance policies are structured around the specific financial architecture of high-end travel, where cancellation penalties are steep, deposits are large, and the gap between what you paid and what you might recover without insurance is enormous.

What trip cancellation and interruption coverage actually protects

Trip cancellation coverage reimburses 100% of your prepaid, non-refundable costs if you have to cancel before departure for a covered reason, whether that is a medical emergency, a family bereavement, or a severe weather event. Trip interruption coverage goes further. Plans like the AXA Explorer Elite reimburse up to 150% of your prepaid trip costs if your trip is cut short, covering not just what you lost but also the additional expenses of getting home early or rebooking segments mid-trip.

That 150% figure matters more than most travelers realize. If you are two weeks into a month-long trip and a medical event forces you home, you are not just losing the remaining prepaid costs. You are also paying for emergency flights, last-minute hotel nights, and rebooking fees. The interruption benefit absorbs all of that.

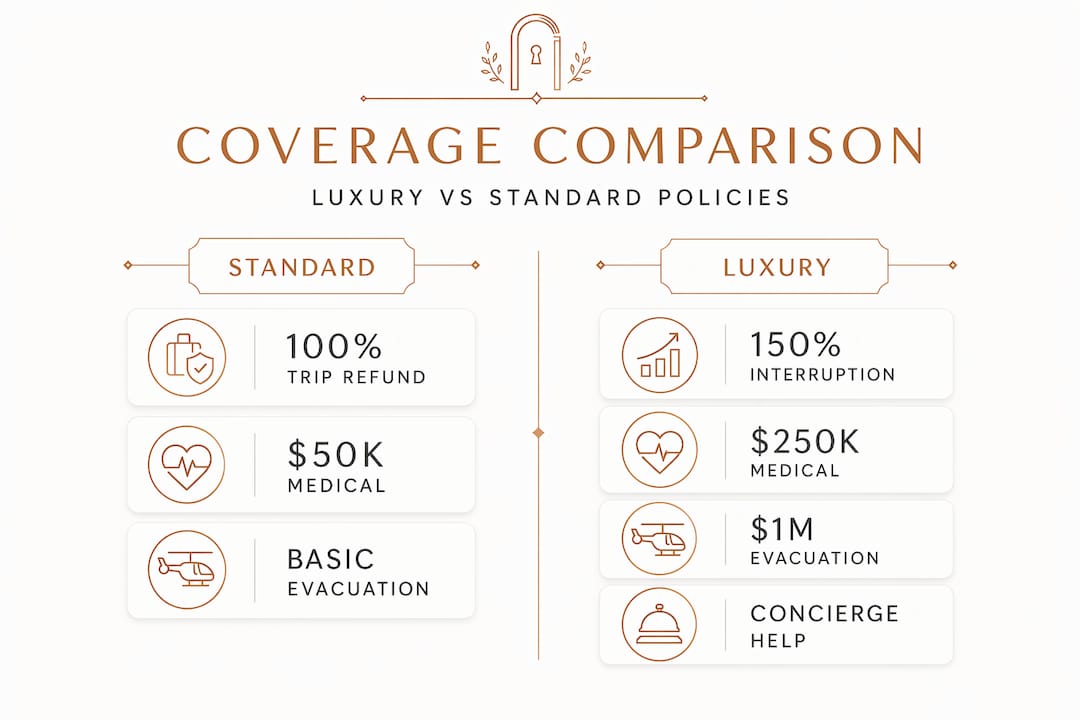

| Plan feature | Standard coverage | Luxury coverage |

|---|---|---|

| Trip cancellation | Up to 100% of trip cost | 100% of trip cost |

| Trip interruption | 100–125% of trip cost | Up to 150% of trip cost |

| Medical coverage | $50,000–$100,000 | $250,000+ |

| Evacuation coverage | $250,000–$500,000 | Up to $1,000,000 |

| CFAR option | Rarely available | Standard upgrade option |

Pro Tip: Always confirm that your policy’s trip cancellation limit matches your total prepaid trip cost. Many travelers accidentally underinsure by forgetting to include private transfers, pre-booked tours, and resort fees.

Medical and evacuation coverage abroad

This is where the importance of luxury travel insurance becomes impossible to ignore. Medical emergencies abroad are not just stressful. They are expensive in ways that can permanently damage your finances. Average medical claims for serious illness or injury during travel average near $28,000, with acute events requiring ICU care exceeding $40,000. And that is before factoring in medical evacuation costs, which can run $100,000 or more depending on your location.

Top luxury plans address this directly. The AXA Explorer Elite, for example, offers $250,000 in emergency medical coverage and up to $1,000,000 in medical evacuation coverage. Those limits are not arbitrary. They reflect the real cost of being airlifted from a remote destination to a hospital equipped to handle a cardiac event or a serious trauma injury.

Here is what comprehensive medical coverage actually delivers:

- Emergency medical treatment: Covers hospitalization, surgery, specialist care, and prescription costs abroad without requiring you to pay out of pocket first.

- Medical evacuation: Arranges and funds transport to the nearest appropriate medical facility or, when medically necessary, back to your home country.

- Cashless hospital access: Top plans work with hospital networks directly, so you are not filing reimbursement claims from a hospital bed in a foreign country.

- 24/7 medical assistance lines: Connects you with medical professionals who can advise on local care options, coordinate with treating physicians, and manage logistics in real time.

- Repatriation of remains: A coverage category no one wants to think about but every serious traveler should confirm is included.

Emergency medical claims are primarily driven by severe illness and injuries requiring hospitalization or ICU care. The practical implication is clear: a $50,000 medical limit is not adequate for a luxury traveler heading to a remote destination. You need coverage that matches the actual cost of the worst-case scenario.

Pro Tip: If your itinerary includes adventure activities like heli-skiing, diving, or off-road expeditions, verify that your policy covers those activities specifically. Many standard plans exclude high-risk pursuits even at the luxury tier.

Cancel For Any Reason: flexibility with fine print

Cancel For Any Reason (CFAR) is the most requested upgrade in travel insurance for high-end vacations, and also the most misunderstood. The appeal is obvious. Standard cancellation coverage only pays out for specific covered reasons. CFAR lets you cancel for any reason at all, no questions asked. The trade-off is partial reimbursement and strict timing rules.

CFAR coverage reimburses 50–75% of your prepaid, non-refundable trip costs. It must be purchased within 14–21 days of your initial deposit, you must insure 100% of your prepaid trip expenses to qualify, and you must cancel at least 2–3 days before your scheduled departure. Miss any one of those conditions and the benefit disappears.

“CFAR is not a last-minute safety net. It is a time-sensitive decision that needs to be made at the moment you commit to the trip, not the week before you leave.”

The most common mistake luxury travelers make with CFAR is treating it like a purchase they can make later. By the time uncertainty sets in about a trip, the purchase window has almost always closed. The initial purchase window is typically 14–21 days after your first deposit, which for a luxury trip might be 12 to 18 months before departure.

A few additional points worth understanding before selecting luxury travel insurance with CFAR:

- CFAR does not replace standard cancellation coverage. It supplements it for situations that fall outside covered reasons.

- The 50–75% reimbursement rate means you will absorb some loss. On a $50,000 trip, that could still mean recovering $25,000 to $37,500.

- Insuring the full trip cost is not optional. Partial coverage invalidates CFAR eligibility entirely.

Concierge and assistance services

Money limits on a policy tell one part of the story. The concierge and assistance services that come with premium luxury trip insurance policies tell the rest. For a traveler with a tightly scheduled, multi-segment itinerary spanning five countries and three continents, the ability to make one call and have a team handle everything is not a minor perk. It is the difference between a disruption that costs you two days and one that costs you the entire trip.

Here is what top-tier assistance services actually manage:

- Itinerary rebooking: When a flight cancellation or medical delay disrupts your schedule, the assistance team contacts hotels, tour operators, and private transfer companies to rebuild your itinerary in real time.

- Cashless hospital coordination: Rather than paying upfront and filing claims later, the insurer communicates directly with the hospital, handling billing and authorization so you can focus on recovery.

- Lost document and baggage recovery: The team files reports, contacts local authorities, coordinates with airlines, and arranges emergency travel documents when passports or luggage go missing.

- Multilingual 24/7 helplines: For travelers in non-English-speaking destinations, having a support team that communicates in the local language with local medical providers is genuinely valuable.

- Medical paperwork management: Overseas medical bureaucracy is complex. Assistance teams handle authorizations, translations, and claims documentation so nothing falls through the cracks.

Luxury travel insurance that includes continuous assistance functions as a travel management resource, not just a financial safety net. For complex itineraries where one missed connection can cascade into a week of disruption, that operational support is often what travelers remember most. The 24/7 multilingual support capacity to navigate complex medical and travel logistics overseas is a defining feature of top-tier luxury plans.

Selecting luxury travel insurance

Knowing the benefits of travel insurance is one thing. Choosing the right policy for your specific trip is another. The evaluation process for travel insurance for luxury travelers should be methodical, not rushed.

Start with these core considerations:

- Total insured amount: Add up every prepaid, non-refundable expense, including flights, accommodations, private tours, transfers, and dining reservations with deposits. 85% of high-net-worth travelers plan to increase travel spending, which means the financial exposure keeps growing. Your coverage limit must match your actual exposure.

- Medical and evacuation limits: Assess your destination. Remote locations in Southeast Asia, Africa, or South America often require evacuation to reach adequate medical care. A $1,000,000 evacuation limit is not excessive for those destinations.

- High-value belongings: If you are traveling with jewelry, photography equipment, or luxury goods, confirm that your policy’s baggage coverage reflects their actual value. Most standard plans cap baggage at $2,500 or less.

- Activity coverage: Confirm that every planned activity, from scuba diving to horseback riding to helicopter tours, is explicitly covered.

- Claims process: Read reviews specifically about claims handling. A policy that pays out smoothly is worth more than one with better limits that fights every claim.

Pro Tip: When comparing travel insurance options, look beyond the premium cost. A policy that costs 8% of your trip but covers 150% trip interruption and includes CFAR is almost always better value than one at 5% that caps interruption at 100% and excludes flexibility upgrades.

Hiddendoortravel’s luxury travel experts work through these considerations with clients as part of the trip planning process, not as an afterthought. Getting the coverage right from the start is part of building a trip that holds up under any circumstance.

My perspective on what insurance actually does for luxury travelers

I have worked with enough luxury travelers to know that the ones who resist buying comprehensive insurance are almost always the ones who have never had a trip go seriously wrong. The first time a medical emergency forces an early evacuation from a remote destination, or a family situation requires canceling a $60,000 trip with two weeks’ notice, the conversation about insurance changes completely.

What I have found is that the financial reimbursement is rarely the part travelers remember most. It is the 3 a.m. phone call that gets answered by someone who speaks the local language, knows which hospital to call, and has already started the paperwork. That is the part that actually makes a difference when you are scared and far from home.

The mistake I see most often is treating CFAR as something to think about later. By the time most travelers revisit their insurance options, the purchase window has closed and the flexibility is gone. The second most common mistake is insuring only the flights and forgetting that the private villa deposit, the chartered boat, and the curated tour fees are all at risk too.

My honest take: for any luxury trip where the total prepaid costs exceed $15,000, comprehensive coverage with high medical limits, evacuation coverage, and CFAR is not optional. It is the only rational choice. The premium is a small fraction of what you stand to lose, and the assistance services alone are worth the cost on a complex international itinerary.

— Michael

Plan your luxury trip with the right protection in place

At Hiddendoortravel, we build bespoke luxury itineraries where every detail is considered, including how your trip is protected. Our team understands the financial architecture of high-end travel and can guide you toward coverage that matches your actual exposure, destination risks, and travel style.

Whether you are planning a private expedition, a villa stay, or a multi-country cultural tour, we factor insurance considerations into the planning process from day one. Explore our luxury travel services and connect with an expert who can help you build a trip that is as protected as it is extraordinary. For travelers who want inspiration alongside protection strategy, our trip inspiration library is a strong starting point.

FAQ

What does luxury travel insurance typically cost?

Luxury travel insurance typically costs 4–10% of your total trip expenses. On a $40,000 trip, that means a premium of $1,600 to $4,000, which covers 100% trip cancellation and up to 150% trip interruption.

Does luxury travel really need insurance?

Yes. The financial exposure on a luxury trip, where prepaid, non-refundable costs can reach tens of thousands of dollars, makes comprehensive coverage a practical necessity rather than an optional add-on.

What is Cancel For Any Reason coverage and when should I buy it?

CFAR reimburses 50–75% of prepaid trip costs for any cancellation reason. It must be purchased within 14–21 days of your initial deposit, so the decision needs to be made at the time you commit to the trip.

How much medical coverage do luxury travelers need?

Top luxury plans offer $250,000 in emergency medical and up to $1,000,000 in evacuation coverage. For remote destinations, high evacuation limits are especially important given the cost of airlifting a patient to adequate care.

What do concierge services in luxury travel insurance actually do?

Concierge and assistance services coordinate itinerary rebooking, medical logistics, lost document recovery, and cashless hospital access, providing operational support that goes well beyond financial reimbursement.